Heil- und Kostenplan explained: Germany's dental cost plan in English (2026)

If you've just been handed a pink form by your German dentist and you're staring at it wondering what on earth it means — you're in the right place.

A Heil- und Kostenplan (HKP) is a treatment and cost plan that your dentist prepares before any major dental work. It details what treatment you need, what it will cost, and how much your health insurance will cover.

This document must be submitted to your public health insurance or private health insurance provider for approval before treatment can begin. For public insurance patients, you'll usually receive two cost plans (HKP I and HKP II), while private insurance patients typically receive one.

In this guide, we'll walk through every section of the form, explain the approval process step by step, and show you what you'll actually end up paying.

What is a Heil- und Kostenplan?

The Heil- und Kostenplan — literally "healing and cost plan" — is a standardized document required by German law whenever a dentist plans to perform dental prosthetic work (Zahnersatz). It serves two purposes:

- For you: It gives you a detailed cost breakdown so you know what to expect before committing to treatment.

- For your insurer: It allows them to calculate and confirm the subsidy (Festzuschuss) they'll contribute toward your treatment.

The form is issued by the KZBV (Kassenzahnärztliche Bundesvereinigung), Germany's national association of statutory health insurance dentists. Every dentist in Germany uses the same standardized form, so once you understand one, you'll be able to read any Heil- und Kostenplan you receive in the future.

When is a Heil- und Kostenplan required?

An HKP is required before any dental prosthetic treatment (Zahnersatz). This includes:

- Dental crowns

- Dental bridges

- Dental implants

- Dentures (full and partial)

- Inlays and onlays (in some cases)

An HKP is not required for:

- Routine teeth cleanings (Professionelle Zahnreinigung)

- Cavity fillings

- Tooth extractions

- Standard checkups

- Orthodontic treatment (this uses a separate approval process)

If your dentist recommends any form of Zahnersatz, they are legally required to prepare an HKP before starting treatment.

The HKP process: step by step

Here's what happens from the moment your dentist identifies the need for dental prosthetic work to when treatment begins:

1. Dental examination and diagnosis

Your dentist examines your teeth and determines that you need prosthetic work — for example, a crown to protect a damaged tooth, or a bridge to replace a missing one.

2. Dentist prepares the HKP

Your dentist fills out the standardized Heil- und Kostenplan form. This includes recording your current dental status, the proposed treatment (both the standard care option and any preferred alternatives), and the estimated costs.

3. You review and sign

Your dentist explains the treatment options and costs. You sign the form to confirm you've been informed. This is a good time to ask questions — especially about the difference between the standard treatment (which insurance subsidizes) and any upgrades you might prefer.

4. Submission to your insurer

Your dentist submits the signed HKP to your public health insurance provider (Krankenkasse). Some insurers now accept digital submissions, but many still require the physical form.

5. Approval (typically 3-4 weeks)

Your insurer reviews the plan and calculates your Festzuschuss (fixed subsidy). For straightforward treatments, approval usually takes 3 to 4 weeks. For complex or expensive treatments, the insurer may request a review by an independent expert (Gutachter), which can extend the timeline.

Once approved, you'll receive a confirmation showing exactly how much your insurer will cover and how much you'll need to pay out of pocket.

6. Treatment begins

After approval, you can schedule the treatment with your dentist. The approved HKP is typically valid for 6 months — treatment must begin within this window. If the treatment plan changes significantly after approval, a new HKP must be submitted and re-approved.

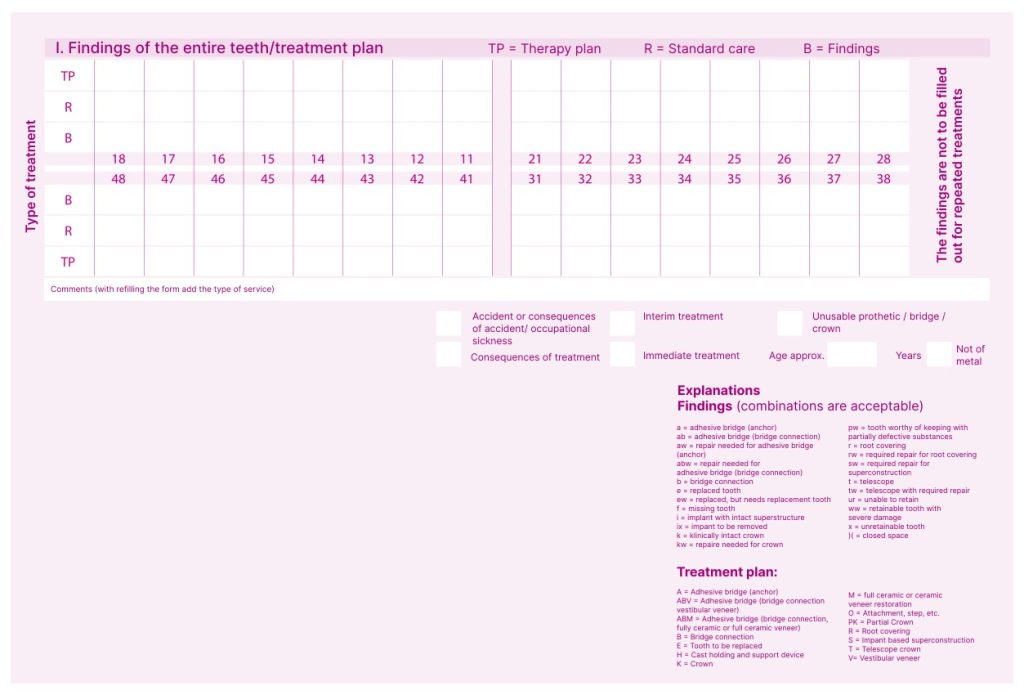

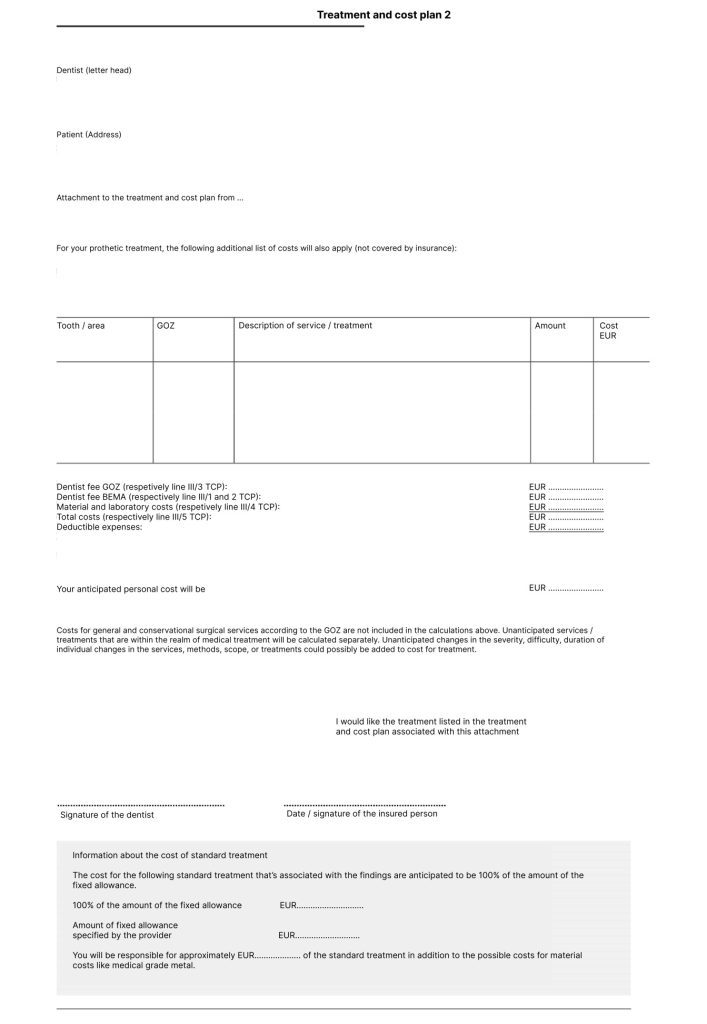

Understanding the pink form (HKP I): section by section

The HKP I is the main cost plan — the pink form you'll receive from your dentist. Here's what each section means:

Section 1: Personal information

The first section covers your basic details: your name, date of birth, health insurance provider, and your dentist's information. You'll sign here to confirm that the information is correct. This section is administrative — it won't affect your treatment costs.

Section 2: Dental findings and treatment plan

This is where your dentist records the current state of your teeth using standardized abbreviations:

- Lowercase letters represent current problems (findings)

- Uppercase letters represent the planned treatments

There are two columns to note: the Regelversorgung (standard care — what public insurance considers adequate) and the therapiegeeignete Versorgung (your dentist's recommended treatment, which may go beyond standard care).

The difference between these two is important: your insurance subsidy is always based on the Regelversorgung, even if you choose a better option.

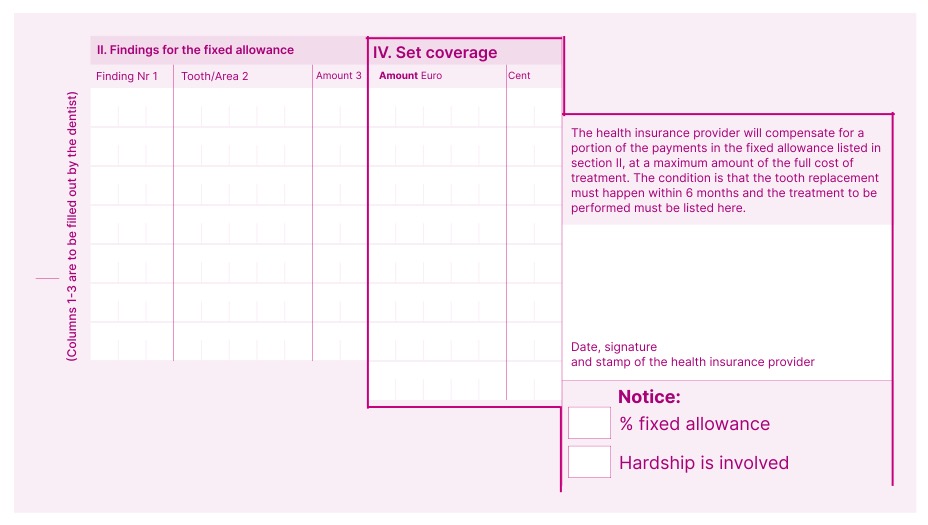

Section 3: Coverage — what's insured vs. what isn't

This section shows which treatments fall under the standard care covered by public health insurance and which don't.

Here's a common scenario: one of your back teeth dies and needs to be replaced. Public health insurance would cover a metal bridge attached to the neighboring teeth — this is the Regelversorgung. But a dental implant, which is usually the better long-term option, goes beyond standard care. If you choose the implant, your insurer still pays the same Festzuschuss (based on the bridge cost), but you cover the rest yourself.

The same applies to cosmetic choices. For example, a fully metal bridge is 100% standard care, but a tooth-colored composite bridge costs more — your Festzuschuss stays the same, and you pay the difference.

This is where supplemental dental insurance becomes valuable: it can cover the gap between what public insurance subsidizes and what your preferred treatment actually costs.

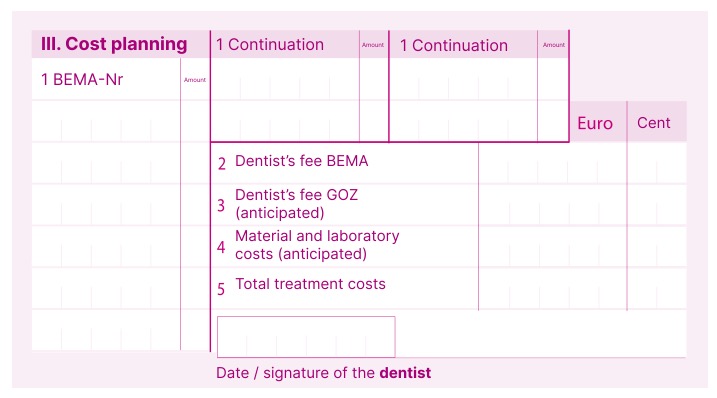

Section 4: Fee schedules (BEMA vs. GOZ)

Dentists in Germany don't set their own prices. They follow standardized fee schedules:

- BEMA (Bewertungsmaßstab zahnärztlicher Leistungen): The fee schedule for treatments billed through public health insurance. All standard care treatments are billed under BEMA.

- GOZ (Gebührenordnung für Zahnärzte): The fee schedule for private or self-pay treatments. GOZ applies when you choose a treatment that goes beyond what BEMA covers — or if you're privately insured.

GOZ fees use a multiplier system (Steigerungsfaktor). The standard multiplier is 2.3x, but dentists can charge between 1.0x and 3.5x depending on the complexity. If your dentist charges above 2.3x, they must provide a written explanation.

For example, the same diagnostic work would be listed as:

| BEMA (public insurance) | GOZ (private/self-pay) |

|---|---|

| BEMA Pos. 4 — PA Status | GOZ 4000 — PA-Status, GOZ 4005 — Erhebung Gingivalindex |

| BEMA Pos. P200 | GOZ 4070 oder Implantat |

If you're publicly insured and choose only the standard treatment, everything stays under BEMA. The moment you opt for an upgrade (like an implant instead of a bridge), the additional treatment is billed under GOZ.

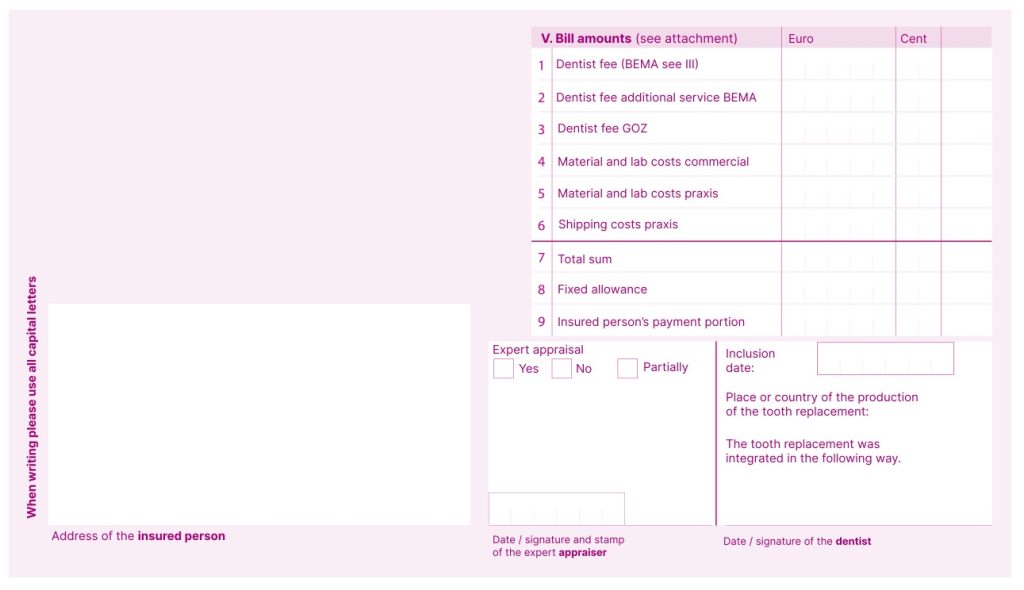

Section 5: Final billing

The final section shows the total amounts — what your insurance covers, what you pay, and the combined BEMA/GOZ charges. It also includes confirmation signatures from your dentist and, in some cases, from your insurer's appraiser (Gutachter).

If the treatment plan changes after approval, the entire HKP must be redone and resubmitted. This resubmission typically takes another 3-4 weeks for approval.

The second cost plan (HKP II): private treatments

If your chosen treatment includes work that goes entirely beyond what public insurance covers, your dentist will prepare a second form: the HKP II (also called the Privatplan or Zusatzplan).

This covers treatments like:

- Implants instead of bridges

- Veneers

- All-ceramic or zirconia crowns when metal would be the standard option

- Other treatments outside the Regelversorgung

If you have supplemental dental insurance, submit the HKP II to your supplemental insurer as well — they'll confirm what additional amount they'll cover.

Note: purely cosmetic treatments (like veneers for aesthetic reasons only) are generally not covered even by supplemental dental insurance.

How much will you actually pay?

Your out-of-pocket cost depends on three things: the Festzuschuss from your public insurer, your Bonusheft status, and whether you have supplemental dental insurance.

How the Festzuschuss (fixed subsidy) works

Public health insurance in Germany doesn't cover a percentage of your actual treatment cost. Instead, it pays a Festzuschuss — a fixed subsidy calculated based on the standard care (Regelversorgung) for your diagnosis.

The base Festzuschuss covers 60% of the Regelversorgung cost. This percentage increases if you've maintained a Bonusheft:

| Bonusheft status | Festzuschuss coverage |

|---|---|

| No Bonusheft or < 5 years | 60% of Regelversorgung |

| 5+ consecutive years | 70% of Regelversorgung |

| 10+ consecutive years | 75% of Regelversorgung |

Cost examples for common treatments

Here's what you'd typically pay for common dental prosthetic treatments, assuming no supplemental insurance:

| Treatment | Total cost (approx.) | Regelversorgung cost | Festzuschuss (60%) | You pay |

|---|---|---|---|---|

| Metal crown (standard care) | ~EUR 400 | EUR 400 | ~EUR 240 | ~EUR 160 |

| Ceramic crown | ~EUR 800 | EUR 400 | ~EUR 240 | ~EUR 560 |

| Metal bridge (3 teeth) | ~EUR 800 | EUR 800 | ~EUR 480 | ~EUR 320 |

| Dental implant (single) | ~EUR 2,500 | EUR 400* | ~EUR 240 | ~EUR 2,260 |

*For implants, the Festzuschuss is based on the bridge that would be the Regelversorgung — not the implant cost.

With a 10-year Bonusheft, the crown example drops from EUR 160 to ~EUR 100 out of pocket. Over multiple treatments, this adds up significantly.

With supplemental dental insurance, many of these out-of-pocket costs can be reduced to zero or near-zero — especially for treatments like ceramic crowns and bridges. Check whether dental insurance is worth it for your situation.

How the Bonusheft (bonus booklet) saves you money

The Bonusheft is a small booklet that your dentist stamps each time you attend a checkup. It's free — ask any dentist for one.

Here's how it works:

- Adults need to visit the dentist at least once per year to get a stamp

- Children and teenagers (under 18) need two visits per year

- After 5 consecutive years of documented checkups, your Festzuschuss rises from 60% to 70%

- After 10 consecutive years, it rises to 75%

If you've just moved to Germany, you can ask your dentist to backdate entries based on records from your previous dentist — even from abroad, as long as you have documentation.

If you're on a tight budget and qualify as a hardship case (Härtefall) — for example, if you receive unemployment benefits or social assistance — your public insurer may cover up to 100% of the Regelversorgung cost.

Your current Bonusheft percentage is shown on the HKP under the "Festzuschuss" line. Make sure it's accurate before your dentist submits the form.

For more on how this works alongside other health insurance benefits, see our guide to the health insurance bonus program.

HKP for private insurance patients

If you have private health insurance, the cost plan process works differently:

- No HKP I / HKP II split: Your dentist prepares a single cost estimate based on the GOZ fee schedule

- No Festzuschuss: Private insurers reimburse based on your policy terms (typically 70-100% of treatment costs, depending on your plan)

- Reimbursement model: You typically pay the dentist directly and submit the invoice to your insurer for reimbursement

- Cost plan requirement: Many private insurers require a cost plan for treatments above a certain threshold — for example, Feather's private health insurance requires one for treatments over EUR 2,500. Without it, reimbursement above that limit may drop to 50%

If you have expat health insurance, check your specific policy terms. Some expat plans have waiting periods for dental prosthetic work and annual limits on coverage.

Whether you're publicly or privately insured, never start expensive dental treatment without getting cost plan approval first. It's the single most important step to avoiding surprise bills.

What if you disagree or want a second opinion?

You have several rights as a patient when you receive a Heil- und Kostenplan:

Get a second opinion: You can take your HKP (or just your dental records) to another dentist for a second opinion on the diagnosis and proposed treatment. This is your right under German patient protection law, and your insurance should cover the consultation.

Request a Gutachter review: If your insurer questions the treatment plan, they may request an independent expert (Gutachter) review. You can also request this yourself if you believe the proposed treatment is excessive or insufficient.

Compare treatment options: Your dentist is legally required to inform you about the standard care option (Regelversorgung) and any alternatives. Ask specifically: "What would the standard treatment be, and what are the pros and cons compared to what you're recommending?"

Negotiate payment: If you can't afford the full out-of-pocket amount, many dental practices offer installment payment plans. Ask before treatment begins.

Validity window: Remember that an approved HKP is valid for approximately 6 months. If you need time to decide, get a second opinion, or arrange financing, you have this window before needing to start treatment.

Your guide to dental care in Germany

Watch our breakdown of how dental care actually works here — what public health insurance pays for, what it doesn't, what major procedures cost out of pocket, and how to keep your bills down.

Sign up for dental insurance

In less than 5 minutes, all online.

Don't take our word for it

Clear advice, kind support

“Booked a call about dental insurance, and Vinny explained everything I needed to know. Thank you.”

Zohara

Simple, fast and trustworthy

“Better dental insurance than its alternatives.”

Yuna

Quick refunds, great service

“Feather dental insurance is excellent. Refunds were easy and support was amazing.”

Coco