If you have private health insurance, then you may have already received unpleasant news in the mail: your monthly premium is going up. And if you’ve been with the same insurer for awhile, then it may be a substantial price increase.

There are three main reasons why your premium may be adjusted: medical cost increases; adjustments to life expectancy projections; and changes in interest rates. We’ll help you understand the reason for the increase and answer some common questions.

Rising medical costs

This is pretty simple: the cost of high-quality care in advanced health systems like Germany’s is high. A great deal of research and labor goes into implementing advancements in medicines and medical technologies that keep us healthy and save lives—and this is paid for by consumers of the health system, either through contributions to the public Krankenkassen or through monthly premiums paid to private insurers.

There is a major difference in the way these cost increases are reflected in the public and private systems though: public insurers can adjust their prices more frequently—usually each year. So let’s say the cost of medicines and supplies was determined to have increased by 1% a year in 2018 and 1.5% in 2019. The public system would have made adjustments in kind at the beginning of 2019 and 2020, respectively.

For most new policies, premium adjustments can occur only once medical costs are estimated to be at least 5% higher than when the policyholder’s coverage began (or when the last adjustment was made).

Private insurers, however, are only allowed to make adjustments under very specific circumstances. For most new policies, premium adjustments can occur only once medical costs are estimated to be at least 5% higher than when the policyholder’s coverage began (or when the last adjustment was made). Let’s say you signed a private policy in 2018. With the same medical cost increases mentioned above, the 5% mark wouldn’t have been reached—and the insurer must carry these cost increases until that benchmark is hit.

So when private insurers adjust your policy rate, this is usually a reflection of increases over the last four or five years. That means you won’t see premium adjustments so often—but when you do, it’s likely to be a bigger jump than you might see among public insurers. However, if you average out yearly public contribution increases over that same four- or five-year period, you’ll likely find that they’re comparable to your private insurer’s adjustment.

Public or private insurance—which should you choose?

Try our recommendation tool.

Life expectancy projections

Health insurance costs are partly determined by life expectancy tables (commonly known by the more macabre term “mortality tables”). These tables help insurers create a budget for their customers: how much care is a person expected to need for the rest of their life? And how much will that care cost?

As life expectancy rates increase, so do insurance costs. Let’s say someone started coverage when they were 30 years old and their life expectancy at the time was projected to be 84 years old. But now, 10 years later, advancements in medicine mean the life expectancy for that same person is projected at 86 years old.

That’s two years more to live—but those years will be later in life, when care is usually the most expensive. Both public and private insurers cope with these life expectancy increases by making periodic adjustments to monthly premiums or contributions.

Again, the magic 5% number reigns supreme here: if life expectancy projections change more than 5% since coverage began (or since the last adjustment was made), then the premium can be adjusted.

Changes in interest rates

Low interest rates are great for some things. Want a mortgage? A car loan? A new credit card? Then you’re probably searching for the lowest interest rate possible. Indeed, Germany’s low interest rates are meant to stimulate consumption and help people better afford long-term investments, like property.

But when it comes to your private health insurance policy, low interest rates can be a disadvantage. As we’ve outlined before, private insurers rely on a system of old age savings to keep premiums down and ensure that their members can still afford insurance in retirement. This means that every month, a portion of the premium you and other members pay is going into a savings account, which is expected to generate returns for everyone in the long run.

Interest rates in Germany (and Europe generally) have been in the negative for the last few years. These negative rates led to an average of approximately €150/person lost on deposits in 2019, according to Deutsche Bank. And this doesn’t look set to change soon: the long-term interest rate stood below -0.5% for all of 2020.

So what does this have to do with your health insurance? The premium you are quoted when you first sign up is based on a projected interest rate for the old age savings. If that rate changes, then your monthly premium may need to be adjusted.

These adjustments may result in higher premiums—but they ensure that there’s enough money in the savings pot to keep you covered as you get older. Interest rate adjustments can only be made in combination with the two aforementioned (life expectancy and medical cost) types of adjustments.

The good news? The interest rate will almost certainly go up over time. And if the interest rates go up, then your health insurance premium may even be lowered to take into account higher returns.

Some FAQs

Here are some of the most commonly asked questions about premium increases:

Will a price increase happen every year?

Generally, price adjustments cannot happen every year due to the 5% change benchmarks mentioned above.

Would choosing public health insurance help me avoid price increases?

Public insurers are able to make adjustments on a yearly basis. Public adjustments occur in three main ways:

- Through general increases to the contribution amounts (as determined by the German government);

- By raising the Zusatzbeiträge (additional contribution fees, which are determined by individual Krankenkassen); or

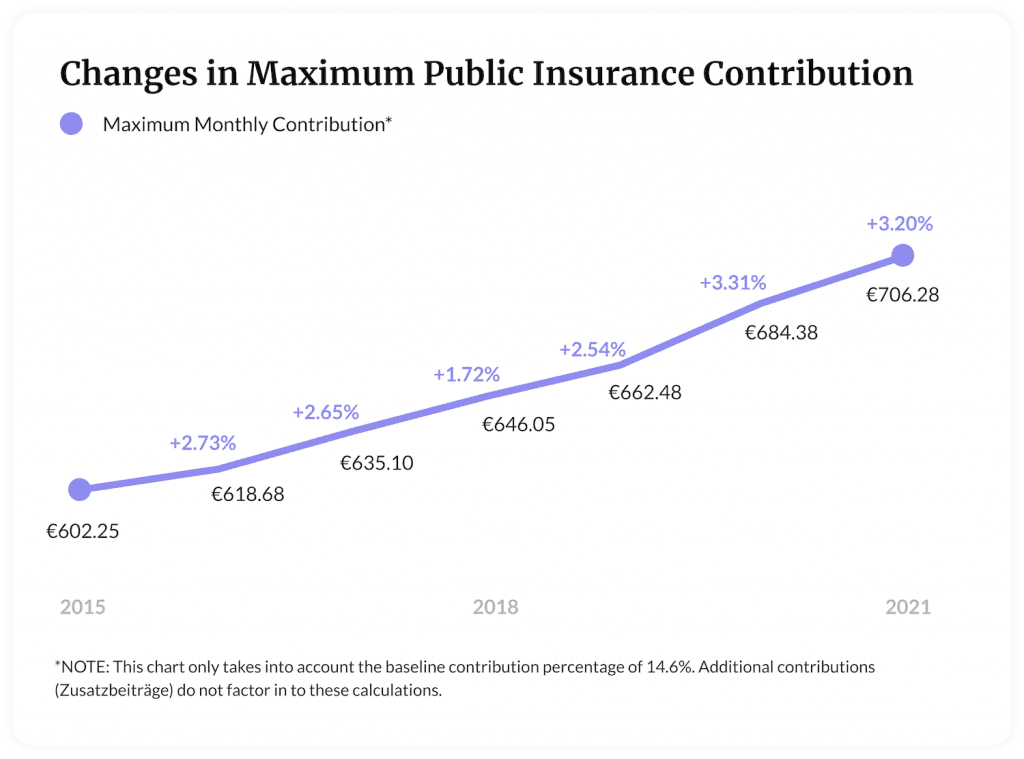

- By raising the Beitragsbemessungsgrenze—the upper salary limit by which maximum contributions are determined. Increases to the Beitragsbemessungsgrenze happen virtually every year. This means that high earners generally end up paying more each year, while contributions for lower earners stay around the same.

In 2015, the Beitragsbemessungsgrenze stood at €4125/month. This put the maximum monthly contribution (at the government-mandated rate of 14.6% of gross income) at €602.25. In 2021, the Beitragsbemessungsgrenze will be €4837.50/month, bringing the maximum monthly contribution up to €706.28—a 17% increase over six years.