Private Pension Germany: The Guide to Retirement

Retirement should be a time of relaxation and enjoyment after years of hard work. Yet concerns about the efficacy of the German pension system can cloud this golden period (there are many myths about pensions in Germany).

In short, statutory pension aims to provide financial security to retirees.

But understanding its details and your options is crucial, especially if you are worried about old age poverty.

Considering private pension schemes as a supplementary option to the statutory pension can enhance your overall retirement income and ensure a more secure financial future.

How old do you have to be to retire in Germany?

You must be 67 to retire in Germany if born after 1964.

However, if you were born before 1964, you could retire earlier:

| Year of Birth | Retirement Age (years and months) |

|---|---|

| from 1964 | 67 years old |

| 1963 | 66 years and 10 months |

| 1962 | 66 years and 8 months |

| 1961 | 66 years and 6 months |

| 1960 | 66 years and 4 months |

| 1959 | 66 years and 2 months |

| 1958 | 66 years and 0 months |

| 1957 | 65 years and 11 months |

| 1956 | 65 years and 10 months |

| 1955 | 65 years and 9 months |

Why is Germany’s retirement age increasing?

The retirement age is increasing because Germany’s population is aging. Hence, more people receive pensions for longer.

Increasing the retirement age allows people to contribute to pensions for longer. Plus, it also ensures that they receive pensions later on.

These changes reduced the financial burden on the statutory pension system. Some say we may see an even greater increase in retirement age in the future.

How does early retirement work in Germany?

You could retire early, starting when you turn 63. That would mean you’d receive a reduced statutory pension.

You can expect your pension to decrease by ≈0.3% for each month of early retirement. This is a rough estimate from our calculations. Use theofficial state pension calculator to see how much your future pension will be.

Early retirement is appealing for those who wish to enjoy their golden years before the rest of the herd.

Still, prepare your retirement funds well in advance. You should account for smaller social security checks and extended retirement years.

How does the statutory German pension system work?

It operates on a principle of solidarity. Contributions from workers fund the statutory pensions of pension insurance system.

Employees and employers contribute a percentage of the former’s salary to the pension fund. Government subsidies also supplement this amount.

In 2025, the contribution rate is 18.6% of gross wages. Employees and employers each contribute 9.3% of the employee’s gross salary.

When it’s your turn to retire, you get monthly payments based on your contribution history.

Overview of the public pension system in Germany

The public pension system in Germany, known as the Gesetzliche Rentenversicherung (GRV), is a cornerstone of the country’s social insurance framework.

This compulsory program ensures that all employees contribute a portion of their earnings to a collective fund, which in turn provides a basic income guarantee for retirees. This contribution is called Rentenversicherung Beitrag, or pension insurance contribution.

Both employees and employers share the responsibility of funding this system, with the government stepping in to provide additional subsidies.

While the GRV is designed to offer a minimum level of income during retirement, it often falls short of maintaining the lifestyle many aspire to.

This is where private pension plans come into play.

By supplementing the public pension system with private pensions, individuals can secure a more comfortable and financially stable future. Private pension plans offer the flexibility and potential for growth that the public system alone may not provide, making them an essential component of a comprehensive retirement strategy.

Why you can’t ignore retirement planning anymore

There are 3 reasons why retirement planning is more critical than ever:

- Future pension benefits are uncertain.

- Career changes happen unexpectedly.

- Retirement should be a time of comfort, not financial stress.

Therefore, it is wise to consider options like a private pension fund to supplement the statutory pension.

Future pension benefits are uncertain.

The sustainability of this pension provision system is under pressure. Germany’s population is aging, and its birth rates are decreasing.

If the imbalance between contributors and beneficiaries grows, younger generations will have to supplement their pension provision with alternative sources of income—for example, personal savings or investment plans.

Also, pension funds rely on their investments’ returns for cash. If they remain too low for too long, they’ll be forced to pause payments or ask the government for a bailout.

Career changes happen unexpectedly.

But what if this scenario doesn’t play out? Still, retirees need financial security if life events reduce their lifetime contributions. Yes, even things you can’t control could reduce your benefits.

Here are some examples:

- Lifetime wages are lower than average.

- Choosing to work part-time.

- Taking a career break.

- Health issues affecting your ability to work.

Retirement should be a time of comfort, not financial stress.

But what if you’re confident in the sustainability of the system? And you know for a fact that you’ll maximize your statutory pension?

Well, you could have to downgrade your lifestyle.

Your pension will be smaller than your current salary unless you supplement it with additional retirement planning.

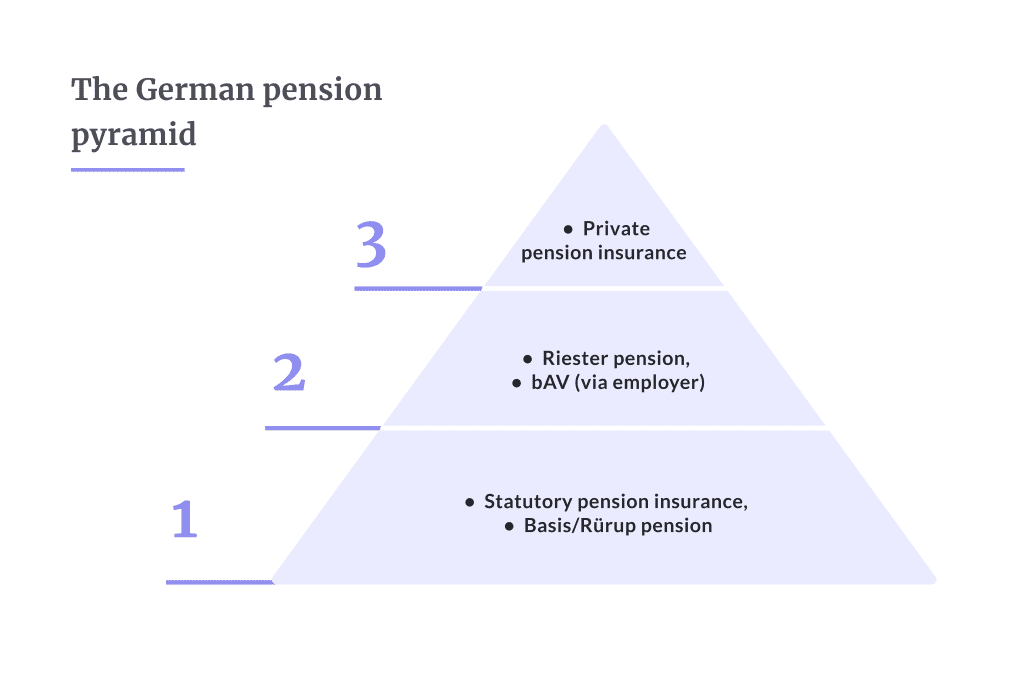

Pension Insurance Options in Germany

By now, you should be convinced that you must plan your retirement.

The German pension system is often compared to a pyramid. There are three levels, and as you go up the pyramid, you increase your financial security. The first level is the basic state pension, which provides a basic level of income in retirement. The second level is occupational pensions, which are provided by employers and include company pension schemes. These schemes often come with added benefits from employer contributions, making them a favorable option for many. The third level is private pensions, individual savings and investment plans.

So, what options are best for you? Let’s find out.

So, what options are best for you? Let’s find out.

What is Basis pension insurance?

The Basic Pension, also known as the “Rürup Rentenversicherung,” after its creator, Bert Rürup, is a pension scheme introduced in Germany in 2005.

The Basis pension is designed to provide long-term financial and social security.

It’s best for the self-employed, freelancers, and high-income earners who aim to stay in Germany their entire career.

How Does It Work?

- Tax Advantages: Contributions made to the Basis pension are tax-deductible.

For example, if you contribute 10’000 € in a year, the government will tax you as if you earned 10’000€ less than you currently do.

Yes, that’s right. You can reduce your taxable income by the amount you contribute! However, note that this only applies to taxable income in Germany. - Lifetime Income: Upon retirement, you’ll receive monthly pension payments in annuity (forever). This is on top of the statutory pension.

- Flexibility: You can choose how much to contribute and how aggressively you want to invest. You can also increase, decrease, or pause your contributions anytime.

- Protection: The basic pension offers total protection against attachment by creditors.

In English? It means you’re shielded from seizures in many circumstances, like bankruptcy.

What’s the catch?

- Eligibility: You must live and pay taxes in Germany. Otherwise, it’s available for everyone.

- Income Limitations: There are no income limitations. But, the tax benefits make it more attractive for higher-income earners in the top tax bracket.

- Long-Term Commitment: You can’t withdraw money or cancel this basic pension policy. You can only pause your contributions (even forever, if you wish) instead of canceling.

Is the Basis pension a good choice for me?

The Basis pension is excellent for self-employed and high-income earners in Germany long term. Its tax advantages and focus on lifetime income make it perfect for increasing retirement income.

However, private pension insurance is the better alternative if you seek flexibility or pursue a career outside of Germany.

What is Riester pension insurance?

The Riester Pension adds to the social security money you get from the state pension by encouraging you to save on your own, thanks to help from the state.

Former labor minister Walter Riester introduced it in 2002, but it’s lost its luster and has found many critics.

How It Works

You contribute 4% of your annual gross income and get a yearly bonus from the government of 175€. If you have children, the government will add 300€ for each child you have.

If you contribute less than 4%, you’ll get some of the government’s contribution but not the full amount.

You also receive limited tax benefits from the money you pay into it. When people retire, they receive a regular payment for life from their Riester plan.

Problems with the Riester Pension

- Too Complicated: Many rules and paperwork discourage many from signing up.

Even once you’ve signed up, the plan is so complicated that it’s hard to understand how to use it best. - High Costs, Low Returns: Riester plans have high management fees. Over time, these fees reduce the amount of money you earn from investments, making the plan less beneficial than alternatives.

- Questionable Effectiveness: If you commit to a Riester pension, its benefits are negligible. They do not make a big enough difference in improving retirement security. Considering all the efforts you’ll go through, it’s one of the least effective schemes for your future savings.

Is the Riester Pension a good choice for me?

In 2025, the Riester pension has many disadvantages, making it attractive only for low-income earners with at least 2-3 children.

What is Company Pension insurance?

Company pension insurance (bAV) is when employees and employers team up to help save for retirement. There are five main types of company pensions in Germany:

- Direct Insurance

- Pensionskasse

- Pension Fund

- Support Fund

- Direct Commitment.

Direct insurance is the most common option, so let’s explore it in more detail. It offers flexible payout options, including receiving your retirement savings as a lump sum or in monthly installments.

How does direct insurance work?

There are two forms of direct insurance:

- Employer-financed company pension insurance: your employer covers all contributions for your future pension. This ensures you receive an extra, lifelong income funded by your employer.

- Company pension through salary conversion: If your employer does not offer the above, you can use your salary. Your contributions are subtracted from your gross pay, so you won’t have to remember to do it. On top of that, your employer must match at least 15% of the sum you invest.

What’s in it for employees?

- Tax Benefits: Money put into company pensions lowers the amount of tax a person pays.

- Flexibility: Occupational pension plans let employees contribute extra money to increase retirement funds.

- Financial Security: Thanks to tax benefits and employer contributions, it’s one of the best ways to ensure you’ll live decently once you retire.

Is direct insurance a good choice for me?

In almost all cases, German occupational pensions are good for employees and employers.

They provide extra money for retirement and encourage loyalty from employees.

As retirement planning becomes more important, occupational pensions are a big part of Germany’s commitment to its workers.

Whether you’re an employee looking for job security or an employer wanting to offer good benefits, understanding and investing in company pensions is a decision for a better future.

What is private pension insurance?

Private pension insurance is a voluntary savings plan designed to build up assets for retirement. These plans offer tax benefits, including no capital gains tax on ETFs during the accumulation phase, and flexibility in payouts.

Here’s what you need to know:

- Voluntary Savings: Participation is optional and allows you to save money for retirement.

- Tax Benefits: Contributions come with tax advantages, helping you save more. Additionally, there is no capital gains tax on ETFs during the accumulation phase, allowing for tax-free growth.

- Flexible Payouts: You can choose between a lifelong pension or a one-time payment, with different payout structures interacting with capital gains tax during the payout phase.

Private pension insurance is a versatile option. It’s perfect for enhancing retirement savings beyond mandatory pension schemes.

How does it work?

The private pension is like a personal savings account for retirement. You contribute money to it regularly, and over time, it grows. When you retire, you receive payments from this account. It could cover your living expenses, go on holiday, or anything you’d like.

Benefits of the private pension:

- Tax benefits: you can choose whether you want a lifelong monthly payout, a payout next to the statutory pension, or a one-off capital payout. In general, this has substantial tax benefits when you retire, including tax-free capital growth during the accumulation phase. This is one of the main reasons private pensions are so efficient at preparing you for the future.

- Flexibility: You have control over how much you contribute and how you invest your money. You can also withdraw some funds at any time for unexpected events.

- Supplementary Income: The private pension supplements your other sources of income and helps ensure a comfortable standard of living in retirement.

What happens with my private pension if I leave Germany?

You don’t have to live in Germany to take part in your pension insurance. You only need a European bank account, and receive tax benefits worldwide.

Is a Private Pension right for me?

We recommend everyone consider private pension insurance. Well, anyone who wants flexibility and a decent standard of living in retirement is the right fit.

Investment options for private pensions

When it comes to private pensions in Germany, a variety of investment options are available to help grow your retirement savings. These options include Exchange-Traded Funds (ETFs), stocks, bonds, and real estate. Each investment vehicle comes with its own set of benefits and risks, allowing you to tailor your private pension plan to your financial goals and risk tolerance.

ETFs are particularly popular for private pensions due to their ability to offer diversification, low fees, and the potential for long-term growth. By spreading your investments across a broad range of assets, ETFs can help mitigate risk while aiming for higher returns. Stocks and real estate, on the other hand, can provide significant growth opportunities but may come with higher volatility and fees. Bonds are generally more stable but offer lower returns compared to stocks and real estate.

Choosing the right mix of these investment options can enhance the yields of your private pension, ensuring that you have a robust financial cushion when you retire.

Role of ETFs in enhancing private pension returns

ETFs play a crucial role in enhancing the yields of private pension plans in Germany. These investment vehicles allow you to invest in a diversified portfolio of assets, which can help increase your long-term returns while reducing risk exposure. ETFs are also cost-effective, with lower management fees compared to mutual funds, making them an attractive option for those looking to maximize their retirement savings.

By including ETFs in your private pension plan, you can benefit from the growth potential of various markets without the need to manage individual stocks or bonds actively. This hands-off approach not only simplifies your investment strategy but also leverages the power of diversification to protect your savings from market volatility.

Investment vehicles and their volatility

Understanding the volatility of different investment vehicles is essential when planning your private pension.

ETFs, for example, offer a balanced approach by providing diversification, which can reduce overall risk compared to investing in individual stocks. However, they are still subject to market fluctuations.

Stocks, while potentially offering higher returns, come with increased volatility and risk.

Real estate investments can provide stability and tangible assets but may involve higher fees and lower liquidity.

Bonds are generally considered safer but offer lower returns, making them a conservative choice for risk-averse investors.

By carefully evaluating the volatility and potential returns of each investment vehicle, you can create a well-diversified private pension portfolio that aligns with your financial goals and risk tolerance.

Calculating your monthly pension income

Calculating your monthly pension income in Germany involves several factors, including your earnings history, contributions to the public pension system, and returns from private pension investments. While this process can be complex, various online pension calculators are available to help you estimate your future income.

These tools take into account your salary, years of contribution, and expected investment returns to provide a rough estimate of your monthly pension.

By using these calculators, you can gain a clearer understanding of how much you need to save and invest to achieve your desired retirement income.

How much pension does a German citizen get?

The amount of pension a German citizen receives varies based on individual circumstances, such as their earnings history and contributions to the public pension system.

On average, retirees can expect to receive around 48% of their last income as a pension. However, this percentage can fluctuate depending on factors like career breaks, part-time work, and overall lifetime earnings.

To bridge the gap between the public pension and your financial needs, private pension plans are essential.

These plans can supplement your basic pension, providing additional income to ensure a comfortable and secure retirement. By strategically combining public and private pension systems, you can optimize your retirement strategy and enjoy peace of mind in your golden years.

Conclusion

Planning for retirement in Germany involves understanding and utilizing various pension options.

While the statutory pension system is essential, supplementing it with private pensions, company schemes, or ETF saving plans enhances your financial security.

With its tax benefits and flexibility, the German private pension is a valuable tool for building additional retirement income.

Whether you’re at the beginning of your career or approaching retirement, integrating these options into your strategy will help ensure a stable and comfortable retirement.

Pension Insurance FAQ

What are ETF plans?

ETFs (Exchange-Traded Funds) are a modern approach to retirement planning. They track the performance of specific indices and offer diversification and potentially higher returns than savings accounts.

ETFs are commonly used in pension plans, but you can invest in them independently.

An ETF saving plan involves making regular contributions to a portfolio of ETFs through a brokerage account. These contributions are invested in a mix of stocks and bonds, potentially growing over time to provide income in retirement.

How do contributions to pension insurance products work?

In almost all pension products, you can choose the monthly contribution entirely. The more you contribute, the more money gets invested and the higher the payout.

How much should you contribute to pension products?

We recommend contributing a total of around 10% of your income after taxes to all retirement saving plans you undertake.

What happens to my pension products if I leave Germany?

This depends on the pension product you have because they work very differently.

- If you have a Basis pension and no more taxable income in Germany: you can still participate without tax benefits.

- If you have Riester Pension insurance and leave Germany: you won’t receive the bonuses the government pays, which makes the Riester pension interesting in the first place.

- If you have Private pension insurance: you don’t have to live in Germany to take part in your pension insurance. You only need a European bank account. You even receive tax benefits worldwide.

Can I get a Refund for my Retirement Contributions?

It’s possible to get your pension back. For other pension products, it depends on what you subscribe to because they work very differently.

- If you have a Basis pension: Contributions to the Basis Pension are intended to be long-term; you can’t withdraw money or cancel the policy. You can only pause your contributions for an unlimited time instead of the cancellation, and you will receive a lifelong pension when you retire.

- If you have a Riester Rente: Getting a refund is possible but not recommended. You will lose all the government bonuses you have collected over the years. And, if you have benefited from the Riester pension for tax benefits, you will have to pay them back.

- If you have a Private Pension: Yes. You can withdraw money from it. Like in every other investment product, you only have to pay taxes on the stock market returns if you withdraw money from it before you retire.

Sign up for pension insurance

All online. Withdraw money anytime.

Frequently asked questions

Don't take our word for it

Experts always helping for pension questions

“Laura explained pension plans clearly and helped me find the best option for my situation.”

Sabina

Clear advice, easy platform

“Feather made pensions easy to understand; and the platform is also very user-friendly.”

Melody

Thank you Laura!

“She went the extra mile to clarify our tricky Basis Pension application.”

Chris